Chapter 2 – Asset Classes and Financial Instruments

CHAPTER 2: ASSET CLASSES AND FINANCIAL

INSTRUMENTS

PROBLEM SETS

1.

Preferred stock is like long-term debt in that it typically promises a fixed payment

each year. In this way, it is a perpetuity. Preferred stock is also like long-term debt

in that it does not give the holder voting rights in the firm.

Preferred stock is like equity in that the firm is under no contractual obligation to

make the preferred stock dividend payments. Failure to make payments does not set

off corporate bankruptcy. With respect to the priority of claims to the assets of the

firm in the event of corporate bankruptcy, preferred stock has a higher priority than

common equity but a lower priority than bonds.

2.

Money market securities are called cash equivalents because of their high level

of liquidity. The prices of money market securities are very stable, and they can

be converted to cash (i.e., sold) on very short notice and with very low

transaction costs. Examples of money market securities include Treasury bills,

commercial paper, and banker’s acceptances, each of which is highly marketable

and traded in the secondary market.

3.

(a) A repurchase agreement is an agreement whereby the seller of a security

agrees to “repurchase” it from the buyer on an agreed upon date at an agreed

upon price. Repos are typically used by securities dealers as a means for

obtaining funds to purchase securities.

4.

Spreads between risky commercial paper and risk-free government securities

will widen. Deterioration of the economy increases the likelihood of default on

commercial paper, making them more risky. Investors will demand a greater

premium on all risky debt securities, not just commercial paper.

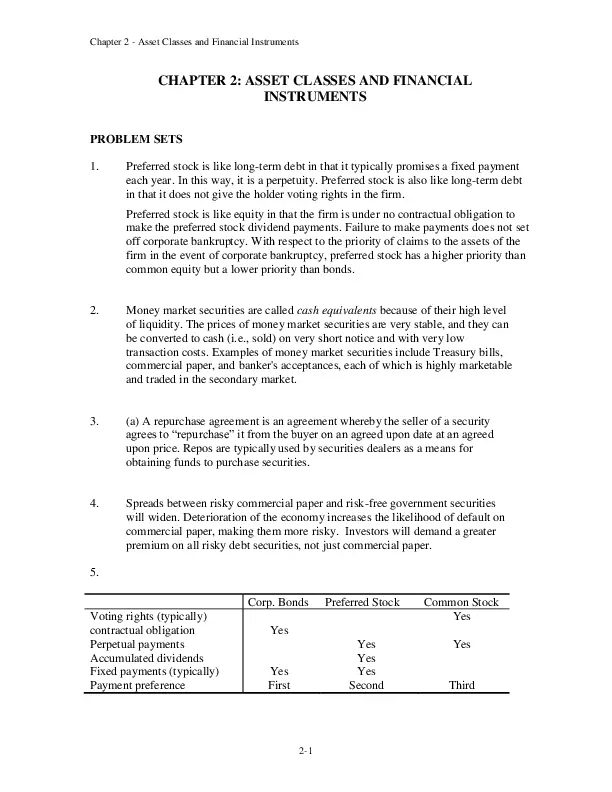

5.

Corp. Bonds

Voting rights (typically)

contractual obligation

Perpetual payments

Accumulated dividends

Fixed payments (typically)

Payment preference

Preferred Stock

Common Stock

Yes

Yes

Yes

Yes

Second

Yes

Yes

Yes

First

2-1

Third

Chapter 2 – Asset Classes and Financial Instruments

6.

Municipal bond interest is tax-exempt at the federal level and possibly at the

state level as well. When facing higher marginal tax rates, a high-income

investor would be more inclined to invest in tax-exempt securities.

7.

a.

You would have to pay the ask price of:

111.8203% of par value of $1,000 = $1118.203

8.

b.

The coupon rate is 3.125% implying coupon payments of $31.25 annually or,

more precisely, $15.625 semiannually.

c.

The yield to maturity on a fixed income security is also known as its required

return and is reported by The Wall Street Journal and others in the financial

press as the ask yield. In this case, the yield to maturity is 2.496%. An investor

buying this security today and holding it until it matures will earn an annual

return of 2.496%. Students will learn in a later chapter how to compute both

the price and the yield to maturity with a financial calculator.

Treasury bills are discount securities that mature for $10,000. Therefore, a specific Tbill price is simply the maturity value divided by one plus the semi-annual return:

P = $10,000/1.02 = $9,803.92

9.

The total before-tax income is $4. After the 70% exclusion for preferred stock

dividends, the taxable income is: 0.30 $4 = $1.20

Therefore, taxes are: 0.30 $1.20 = $0.36

After-tax income is: $4.00 – $0.36 = $3.64

Rate of return is: $3.64/$40.00 = 9.10%

10.

a.

You could buy: $5,000/$142.97 = 34.97 shares. Since it is not possible to trade

in fractions of shares, you could buy 34 shares of GD.

b.

Your annual dividend income would be: 34 $3.04 = $103.36

c.

The price-to-earnings ratio is 15.39 and the price is $142.97. Therefore:

$142.97/Earnings per share = 15.39 Earnings per share = $9.29

d.

General Dynamics closed today at $142.97, which was $0.47 lower than

yesterday’s price of $143.44.

2-2

Chapter 2 – Asset Classes and Financial Instruments

11.

a.

At t = 0, the value of the index is: (90 + 50 + 100)/3 = 80

At t = 1, the value of the index is: (95 + 45 + 110)/3 = 83.333

The rate of return is: (83.333/80) 1 = 4.17%

b.

In the absence of a split, Stock C would sell for 110, so the value of the

index would be: (95+45+110)/3 = 250/3 = 83.333 with a divisor of 3.

After the split, stock C sells for 55. Therefore, we need to find the divisor

(d) such that: 83.333 = (95 + 45 + 55)/d d = 2.340. The divisor fell,

which is always the case after one of the firms in an index splits its

shares.

12.

c.

The return is zero. The index remains unchanged because the return for

each stock separately equals zero.

a.

Total market value at t = 0 is: ($9,000 + $10,000 + $20,000) = $39,000

Total market value at t = 1 is: ($9,500 + $9,000 + $22,000) = $40,500

Rate of return = ($40,500/$39,000) – 1 = 3.85%

b.

The return on each stock is as follows:

rA = (95/90) – 1 = 0.0556

rB = (45/50) – 1 = –0.10

rC = (110/100) – 1 = 0.10

The equally weighted average is:

[0.0556 + (-0.10) + 0.10]/3 = 0.0185 = 1.85%

13.

The after-tax yield on the corporate bonds is: 0.09 (1 – 0.30) = 0.063 = 6.30%

Therefore, municipals must offer a yield to maturity of at least 6.30%.

14.

Equation (2.2) shows that the equivalent taxable yield is: r = rm /(1 – t), so simply

substitute each tax rate in the denominator to obtain the following:

a.

4.00%

b.

4.44%

c.

5.00%

d.

5.71%

2-3

Chapter 2 – Asset Classes and Financial Instruments

15.

In an equally weighted index fund, each stock is given equal weight regardless of its

market capitalization. Smaller cap stocks will have the same weight as larger cap

stocks. The challenges are as follows:

Given equal weights placed to smaller cap and larger cap, equalweighted indices (EWI) will tend to be more volatile than their marketcapitalization counterparts;

It follows that EWIs are not good reflectors of the broad market that they

represent; EWIs underplay the economic importance of larger

companies.

Turnover rates will tend to be higher, as an EWI must be rebalanced

back to its original target. By design, many of the transactions would be

among the smaller, less-liquid stocks.

16.

a.

The ten-year Treasury bond with the higher coupon rate will sell for a higher

price because its bondholder receives higher interest payments.

b.

The call option with the lower exercise price has more value than one with a

higher exercise price.

c.

The put option written on the lower priced stock has more value than one

written on a higher priced stock.

a.

You bought the contract when the futures price was $3.96 (see Table

17.

2.8). The contract closes at a price of $4.06, which is $0.10 more than the

original futures price. The contract multiplier is 5000. Therefore, the gain will

be: $0.08 5000 = $400.00

18.

a.

Owning the call option gives you the right, but not the obligation, to buy at

$150, while the stock is trading in the secondary market at $152. Since the

stock price exceeds the exercise price, you exercise the call.

The payoff on the option will be: $152 – $150 = $2

The cost was originally $3.31, so the profit is: $2 – $3.31 = -$1.31

b.

Since the stock price is greater than the exercise price, you will exercise the call.

The payoff on the option will be: $152 – $145 = $7

The option originally cost $6.60, so the profit is $7 – $6.60 = $.40.

c. Owning the put option gives you the right, but not the obligation, to sell at $155, but

you could sell in the secondary market for $152, if you exercise the call the payoff

on the option will be: $155 – $152 = $3.

2-4

Chapter 2 – Asset Classes and Financial Instruments

The option originally cost $6.53, so the profit is $3-$6.53 = -$3.53.

19.

There is always a possibility that the option will be in-the-money at some time prior to

expiration. Investors will pay something for this possibility of a positive payoff.

20.

a.

b.

c.

d.

e.

a.

b.

c.

d.

e.

Value of Call at Expiration Initial Cost

0

4

0

4

0

4

5

4

10

4

Value of Put at Expiration Initial Cost

10

6

5

6

0

6

0

6

0

6

Profit

-4

-4

-4

1

6

Profit

4

-1

-6

-6

-6

21.

A put option conveys the right to sell the underlying asset at the exercise price. A

short position in a futures contract carries an obligation to sell the underlying asset

at the futures price. Both positions, however, benefit if the price of the underlying

asset falls.

22.

A call option conveys the right to buy the underlying asset at the exercise price. A

long position in a futures contract carries an obligation to buy the underlying asset

at the futures price. Both positions, however, benefit if the price of the underlying

asset rises.

CFA PROBLEMS

1.

(d) There are tax advantages for corporations that own preferred shares.

2.

The equivalent taxable yield is: 6.75%/(1 0.34) = 10.23%

3.

(a) Writing a call entails unlimited potential losses as the stock price rises.

2-5

Chapter 2 – Asset Classes and Financial Instruments

4.

a.

The taxable bond. With a zero tax bracket, the after-tax yield for the

taxable bond is the same as the before-tax yield (5%), which is greater than

the yield on the municipal bond.

b.

The taxable bond. The after-tax yield for the taxable bond is:

0.05

(1 – 0.10) = 4.5%

c.

You are indifferent. The after-tax yield for the taxable bond is:

0.05 (1 – 0.20) = 4.0%

The after-tax yield is the same as that of the municipal bond.

d.

5.

The municipal bond offers the higher after-tax yield for investors in tax

brackets above 20%.

If the after-tax yields are equal, then: 0.056 = 0.08 × (1 – t)

This implies that t = 0.30 =30%.

2-6