CHAPTER 2

Interest Rates

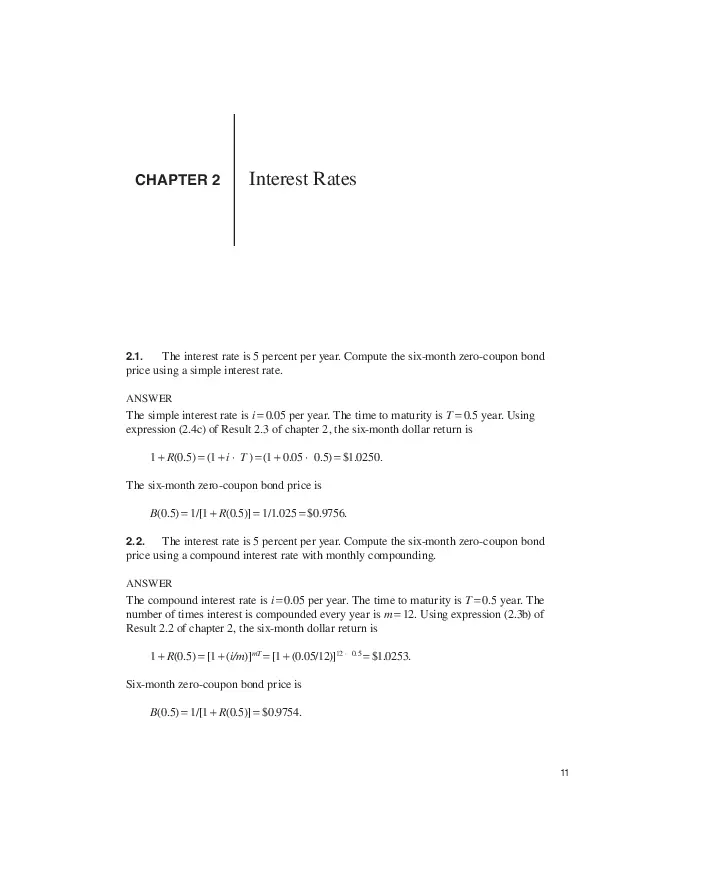

The interest rate is 5 percent per year. Compute the six-month zero-coupon bond

price using a simple interest rate.

2.1.

ANSWER

The simple interest rate is i = 0.05 per year. The time to maturity is T = 0.5 year. Using

expression (2.4c) of Result 2.3 of chapter 2, the six-month dollar return is

1 + R(0.5) = (1 + i × T ) = (1 + 0.05 × 0.5) = $1.0250.

The six-month zero-coupon bond price is

B(0.5) = 1/[1 + R(0.5)] = 1/1.025 = $0.9756.

2.2.

The interest rate is 5 percent per year. Compute the six-month zero-coupon bond

price using a compound interest rate with monthly compounding.

ANSWER

The compound interest rate is i = 0.05 per year. The time to maturity is T = 0.5 year. The

number of times interest is compounded every year is m = 12. Using expression (2.3b) of

Result 2.2 of chapter 2, the six-month dollar return is

1 + R(0.5) = [1 + (i/m)]mT = [1 + (0.05/12)]12 × 0.5 = $1.0253.

Six-month zero-coupon bond price is

B(0.5) = 1/[1 + R(0.5)] = $0.9754.

11

12 | Chapter 2

The interest rate is 5 percent per year. Compute the six-month zero-coupon bond

price using a continuously compounded interest rate.

2.3.

ANSWER

The continuously compounded interest rate is r = 0.05 per year. The time to maturity is

T = 0.5 year. Using expression (2.4d) of Result 2.3 of chapter 2, the six-month dollar return is

1 + R(0.5) = erT = e0.05 × 0.5 = 1.025315.

The six-month zero-coupon bond price is

B(0.5) = 1/[1 + R(0.5)] = $0.9753099.

The interest rate is 5 percent per year. Compute the six-month zero-coupon bond

price using a banker’s discount yield (the zero-coupon bond is a US T-bill with 180 days to

maturity).

2.4.

ANSWER

Expression (2.7b) of chapter 2 gives the T-bill price as

B(0.5) = [1 – (Banker’s discount yield) × T / 360]

= 1 – 0.05 × (180 / 360)

= $0.9750.

2.5.

What is a fixed-income security?

ANSWER

Bonds or loans are called fixed-income securities because they make interest and principal

repayments according to a fixed schedule.

The next three questions are based on the following table, where the interest rate is

4 percent per year, compounded once a year.

Time (in years)

Cash Flows

(in dollars)

0 (today)

−105

1

7

2

9

3

108

Interest Rates | 13

Compute the present value of the preceding cash flows.

2.6.

ANSWER

Let us write the cash flow at time T as C(T ), today’s zero-coupon bond price for a bond

maturing at time T as B(T ), and the dollar return over time T for $1 invested today as

1 + R(T ), where time T stand for times 0 (today), 1, 2, and 3 years.

As the interest rate is 4 percent per year, compounded once a year, dollar return and zerocoupon bond prices are computed as follows:

1 + R(1) = 1 + 0.04 = 1.04,

1 + R(2) = [1 + R(1)]2 = 1.0816,

B(1) = 1 / [1 + R(1)] = 0.961538,

B(2) = 1 / [1 + R(2)] = 0.924556,

and so on.

These values are reported in the following table:

Time

Dollar

Return

(notation)

Dollar

Return

(values)

Zero- Coupon

Bond

(notation)

Zero- Coupon

Bond

(values)

Cash Flow

(notation)

Cash Flow

(values)

0

1 + R(0)

1

B(0)

1

C(0)

−105

1

1 + R(1)

1.04

B(1)

0.961538462

C(1)

7

2

1 + R(2)

1.0816

B(2)

0.924556213

C(2)

9

3

1 + R(3)

1.124864

B(3)

0.888996359

C(3)

108

The present value of the above cash flows is given by

3

∑ B(T )C(T ) = B(0)C(0) + B(1)C(1) + B(2)C(2) + B(3)C(3)

T =0

= 1 × (−105) + 0.9615 × 7 + 0.9246 × 9 + 0.8890 × 108

= 6.0634 or $6.06.

2.7.

Compute the future value of the preceding cash flows after three years.

ANSWER

The future value of the cash flows (given in the table) in three years is obtained by

multiplying the present value determined in 2.6 by the three-period dollar return (which is

the value of $1 invested today for three years):

6.0634 × [1 + R(3)] = 6.0634 × 1.1249 = 6.8205 or $6.82.

14 | Chapter 2

2.8.

What would be the fair value of the preceding cash flows after two years?

ANSWER

The future value of the cash flows (given in the table) in two years is obtained by multiplying

the present value determined in 2.6 by the two-period dollar return:

6.0634 × [1 + R(2)] = 6.0634 × 1.0816 = 6.5582 or $6.56.

Alternatively this is obtained by discounting the cash flow value determined in 2.7 by the

one-period dollar return:

6.8205 / 1.04 = $6.56.

If the price of a zero-coupon bond maturing in three years is $0.88, what is the

continuous compounded rate of return?

2.9.

ANSWER

Result 2.4 of chapter 2 gives the continuously compounded rate of return as

r = (1/T )log(1/B) = (1/3)log(1/0.88) = 0.0426 or 4.26 percent.

2.10.

What are the roles of the primary dealers in the US Treasury market?

ANSWER

The primary dealers (like BNP Paribas, Barclays, Cantor Fitzgerald, and Citigroup) are large

financial firms with whom the New York Fed buys and sells Treasuries to conduct open

market operations that fine-tune the US money supply. These firms regularly participate in

Treasury securities auctions and provide information to the Fed’s open-market trading desk

(see Section 2.6).

What is the when-issued market with respect to US Treasuries? What role does this

market play in helping the US Treasury auction securities?

2.11.

ANSWER

A week or so before a Treasury securities auction, the Treasury announces the size of the

offering, the maturities, and the denominations of the auctioned Treasuries. The Treasury

permits forward trading of Treasury securities between the announcement and the auction,

and the to-be-auctioned issue trades “when, as, and if issued.” Traders take positions in

this when-issued market and a consensus price emerges. The traders in the when-issued

market fulfill their commitments after the Treasuries become available through the

auction. Thus, the when-issued market helps in price discovery and spreads the demand

over seven to ten days, which leads to a smooth absorption of the securities by the market

(see Section 2.7).

Interest Rates | 15

2.12.

What is the difference between on-the-run and off-the-run Treasuries?

ANSWER

Newly auctioned Treasuries are called on-the-run Treasuries. Off-the-run Treasuries are

those issued in prior auctions. On-the-run Treasuries tend to be more liquid market with a

lower spread than off-the-run issues.

2.13.

What is a repurchase agreement? Explain your answer with a diagram of the transaction.

ANSWER

A repurchase agreement (also known as a repo, RP, or sale and repurchase agreement)

involves the sale of securities together with an agreement that the seller buys back

(repurchases) the securities at a later date at a predetermined price.

Consider an example: suppose Repobank takes $50 million from RevRepobank and

sells RevRepobank Treasury securities worth a little more. The next day Repobank

repurchases those securities at a slightly higher price. The extra amount determines an

annual interest rate known as the repo rate. Thus a repurchase agreement is a short-term loan

that is backed by high quality collateral (see the next figure). If Repobank defaults, then

RevRepobank keeps the securities. If RevRepobank fails to deliver the securities instead,

then Repobank keeps the cash longer; the repo is extended by a day, but the terms remain the

same (see Extension 2.4 for further examples and discussion).

An Overnight Repo and a Reverse Repo Transaction

Starting Date (Today)

$50 million

Repobank

RevRepobank

T-securities worth $50 million

Ending Date (Tomorrow)

$50(1 + interest) million

Repobank

RevRepobank

T-securities worth $50 million

16 | Chapter 2

What is a Treasury STRIPS? What benefits do the trading of Treasury STRIPS

provide?

2.14.

ANSWER

US Treasury STRIPS (Separate Trading of Registered Interests and Principal of Securities)

are artificially created zero-coupon bonds. They are created by selling the principal or the

interest payments on a Treasury security (an eligible T-note, or a T-bond, or a Treasury

inflation-protected security) separately. The claims on these cash flows are individual zerocoupon bonds. The Treasury does not create these securities by itself. It allows certain

eligible traders (financial instutions, brokers, and dealers of government securities) to create

them, and it also allows traders to reconstruct the original Treasury security by collecting

and combining the relevant individual STRIPS.

STRIPS have several benefits. They make Treasuries more attractive to investors

leading to greater demand, higher prices, lower yields, and cheaper financing of the national

debt. For example, compared to the demand for purchasing a thirty-year bond with sixty cash

flows, there is greater demand for the same bond with the added flexibility that these cash

flows can be sold as STRIPS. This is because different investors need zeros of different

maturities and this increases the demand for the original security.

Moreover, STRIPS help to identify the term structure of interest rates—a graph that

plots the interest rate on bonds (yield) against the time to maturity. These graphs are

useful for managing interest rate risk (see Section 2.8 and discussions in part IV of the

book).

2.15.

Explain how bbalibor is computed by the BBA.

ANSWER

The major London banks handle deficit or surplus funds by borrowing or lending deposits of

different maturities in this market. A bank with surplus funds lends to another bank for a

fixed time period at the London Interbank Offered Rate (libor). These rates may change

minute by minute, and they may vary from bank to bank, but competition ensures that they

are almost nearly the same at any given point in time.

The British Bankers’ Association (BBA) collects libor quotes from sixteen major banks

for Eurodollar deposit maturities ranging from overnight to a year. The BBA computes

a trimmed average of these libor quotes to compute an index known as bbalibor. The

contributing banks are selected on the basis of: (1) the scale of their market activity, (2) their

credit rating, and (3) their perceived expertise in the currency concerned. Soon after 11 am

London time on every trading day, banks submit confidential annualized interest rate quotes

for various currencies and maturities to BBA’s agent, Thomson Reuters. Thomson Reuters:

(1) checks the data, (2) discards the highest and lowest 25 percent of submissions, and

(3) uses the middle two quartiles to calculate a trimmed arithmetic mean. It publishes and

widely distributes the bbalibor indexes along with the individual banks’ quotes by 12 noon

(see chapter 2, Extension 25.2: “Alleged Manipulation of Bbalibor during 2007–9” for recent

non-competitive behavior in the submission of libor quotes).

Interest Rates | 17

2.16.

What is a Eurodollar deposit, and what is a TED spread?

ANSWER

Eurodollars are US dollar deposits held outside the United States in a foreign bank or a

subsidiary of a US bank. Eurodollar deposits are highly popular in the global markets due to

two benefits: they are dollar deposits and they are free from US jurisdiction.

The BBA collects libor quotes and computes trimmed averages known as bbalibor. Due

to credit risk, the bbalibor for Eurodollars has a higher value than a similar maturity Treasury security. Their difference goes by the name of TED (Treasury-Eurodollar) spread.

What is the difference between Treasury bills, notes, and bonds? What are TIPS, and

how do they differ from Treasury bills, notes, and bonds?

2.17.

ANSWER

The US Treasury issues debt securities with maturities of one year or less in the form of

zero-coupon bonds that do not pay any interest but pay back the principal at maturity. It calls

these securities Treasury bills. It also sells coupon bonds that pay fixed interest (coupons)

every six months and a principal amount (par or face value) at maturity. Coupon bonds with

original maturity of two to ten years are called Treasury notes while those with original

maturity of more than ten years up to a maximum of thirty years are called Treasury bonds.

Investors in Treasury bills, notes, and bonds receive cash flows that remain fixed over

the security’s life. The Treasury also sells inflation-indexed bonds called TIPS (Treasury

Inflation Protected Securities), which are coupon bonds with maturities of five, ten, and

thirty years. TIPS guarantee a fixed real rate of return (which is the nominal rate of return in

dollar terms minus the inflation rate as measured by the consumer price index [CPI] over

their life). This is done by adjusting the principal of the bond each year by changes in the US

CPI. Each year the coupon payment is determined by multiplying the adjusted (and

increasing) principal by the real rate of return. Ordinary Treasury notes and bonds do not

have this CPI adjustment (see Section 2.8).

You bought a stock for $40, received a dividend of $1, and sold it for $41 after five

months. What is your annualized arithmetic rate of return?

2.18.

ANSWER

Assuming five months has T = 5 × 30 = 150 days, Result 2.1 of chapter 2 gives

Annualized rate of return

365 ⎞ ⎛ Selling price + Income − Expenses − Buying price ⎞

=⎛

×

⎟⎠

⎝ T ⎠ ⎜⎝

Buying price

365 ⎞ ⎛ 41+ 1− 40 ⎞

×

=⎛

⎝ 150 ⎠ ⎝

⎠

40

= 0.1217 or 12.17 percent.

18 | Chapter 2

Using the standard demand–supply analysis of microeconomics, explain how a

uniform price auction can generate more or less revenue than a discriminatory auction.

2.19.

ANSWER

Suppose that a fixed quantity Q* units of a good is offered for sale. Its supply curve is

depicted in the diagram by the vertical line SS. The demand is shown by a downward sloping

demand curve DD, which cuts the supply curve at P*. In the demand-supply analysis, buyers

pay the equilibrium price P* and an equilibrium quantity Q* gets sold.

Ideally, the seller would like to make each buyer pay the maximum amount he is

willing to pay (called a buyer’s “reservation price”). To do this the seller can set up a

“discriminatory auction” (DA) where successful bidders pay the amount they have bid.

Assume that this demand curve is depicted by DD. In a DA, the buyer with the highest

reservation price gets the first unit (which would be approximately equal to the intercept of

the DD curve on the vertical axis [point E]), the next person pays a slightly lower price and

acquires the second unit, and so on. Thus the seller captures the “consumer surplus” (given

by the triangle ABE), which is the extra amount that the consumers are willing to pay over

and above the revenue P* × Q* given by the rectangle ABCD.

Discriminatory and Uniform Price Auctions (UPA)

in a Demand- Supply Framework

Price

SS

E

Loss from inability

to discriminate

F

P (UPA)

G

H

Gain from added demand

Demand under UPA

P* A

B

D

C

DD (Demand under DA)

Q*

Quantity

However, a discriminatory auction has a “winner’s curse” problem. If a bidder wants

to make sure that she “wins” the auctioned item, then she is likely to overbid and overpay.

This leads to more cautious bid submissions by the auction participants. It also creates an

environment conducive to collusion and information sharing among the bidders.

A uniform price auction is an alternate format where all successful bidders pay the

highest losing bid (or the lowest winning bid). Wouldn’t a UPA lower revenue because the

seller now gets just the rectangle ABCD? Not necessarily. A change in the rules of the auction

game can cause a change in behavior. A UPA is likely to lead to more aggressive bidding due

to elimination of the winner’s curse. For example, even if you overbid at $100, if all successful

bidders are paying $50 then you also pay $50. Assume that the DD curve in a UPA shifts

Interest Rates | 19

outward and is given by the dashed line in the figure (Demand under UPA). P(UPA) is the

price paid by all successful bidders. The total revenue is given by the rectangle FHCD.

Which auction format raises more revenue? The seller in a DA gets revenue that equals the

quadrilateral EBCD while the seller in a UPA gets the rectangle FHCD. By moving from a DA

to a UPA, the auctioneer gives up the triangle with stripes inside (EGF) but gains the triangle

that is cross-hatched inside (GHB). The area EGF is the loss from the inability to discriminate

across bidders while the area GHB is the gain added from the shift in demand due to the changed

auction mechanism. The revenue implication is unclear. It depends on which triangle is bigger.

The key insight of this analysis is that the bidders’ actions are influenced by the rules of the game.

Suppose that you are planning to enroll in a master’s degree program two years in the

future. Its cost will be the equivalent of $160,000 to enroll. You expect to have the following funds:

2.20.

• From your current job, you can save $5,000 after one year and $7,000 after two years.

• You expect a year-end bonus of $10,000 after one year and $12,000 after two years.

• Your grandparents have saved money for your education in a tax-favored savings account,

which will give you $18,000 after one year.

• Your parents offer you the choice of taking $50,000 at any time, but you will get that

amount deducted from your inheritance. They are risk-averse investors and put money

in ultrasafe government bonds that give 2 percent per year.

The borrowing and the lending rate at the bank is 4 percent per year, daily compounded.

Approximating this by continuous compounding, how much money will you need to borrow

when you start your master’s degree education two years from today?

ANSWER

At time t = 1 year, you expect to have C1(1) = $5,000 (savings) + $10,000 (bonus) + $18,000

(grandparents) = $33,000. Invested at 4 percent, this becomes after another year

C1(2) = C1(1) × One-year dollar return = 33,000 erT = 33,000 × e0.04 × 1 = $34,346.76.

At time t = 2 years, you will have

C2(2) = $7,000 (savings) + $12,000 (bonus) = $19,000.

As your parents’ investment earns just 2 percent, take $50,000 now and invest this at

4 percent for two years. This becomes after two years

C3(2) = C3(0) × Two-year dollar return = 50,000 erT = 50,000 × e0.04 × 2 = $54,164.35.

Thus you expect to have after two years

C(2) = C1(2) + C2(2) + C3(2) = $107,511.11.

As you need $160,000 in two years, you need to borrow 160,000 – 107,511.11 = $52,488.89 at

the time.